The Golden Era of Credit Cards

What the first electronic payments revolution can reveal about the future of BNPL and POS Lending

A quick disclaimer, credit cards and “Buy Now, Pay Later”, BNPL, are not exactly the same thing…

Credit cards are a revolving line of credit, meaning you don’t have to pay off the full balance at the end of a billing period

BNPL is a non-revolving line of credit for a fixed amount (and typically for only one purchase), meaning the balance has to be paid off in full and cannot be increased. The key distinction between BNPL and POS Lending is the nature of the relationship to the merchant. BNPL is merchant agnostic while POS Lending is through a specific merchant

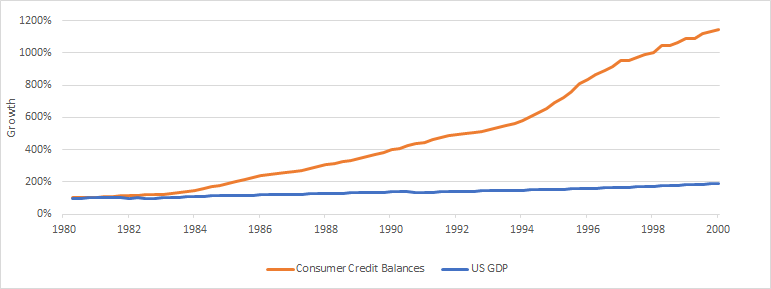

Magnetic Stripes and Reward Programs: Catalysts for Credit Card Growth

In 1980, Visa and Mastercard began issuing cards which utilized the magnetic stripe and POS terminal, created in 1979, which had previously been the exclusive domain of the annual fee paying American Express card holders.

How did a CIA project turn into a catalyst for the growth?

Processing could go digital and be automated

Cost to produce each card dropped from $5 to less than 5¢, which led to the aforementioned Visa and Mastercard adoption of the technology

The two largest POS Terminal manufacturers — Verifone (1981) and Hypercom (1982) — were founded in quick succession leading to an explosion in availability

But looking at the graph, you’re probably wondering “What changed in the mid 1980s?”

One word: Rewards

Reward programs had historically been relegated to stamp books and punch cards and were the exclusive purview of grocers, fuel stations, and department stores. It was the Discover Card (a division of Morgan Stanley) which introduced the first cash back rewards on all purchases in 1986 as an effort to boost adoption of the new network.

Other notable early reward programs:

1987: American Airlines, United, and Delta all introduced airline reward credit card programs changing “the nature of frequent flier programs forever.”

1990: AT&T becomes one of the leading US card issuers in the 1990s after the introduction of the the Universal Card (sold to Citi in 1997) which allowed customer to earn credit against their telephone bills

A subset of reward programs, co-branded credit cards, also brought gas stations back into the card network after a mass exodus from the payment rail in 1979 due to high interchange fees. Co-branded cards allowed merchants to reduce interchange fees while (in theory) driving up revenues.

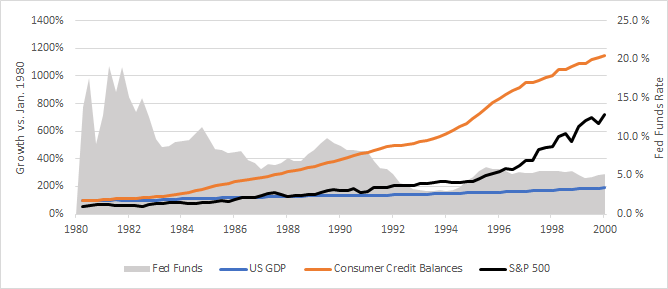

This added fuel (sorry) to the fire leading up to the 1990s as interest rates declined and the economy boomed, leaving banks searching for yield and consumers (many with large savings balances) feeling more confident than ever. The former encouraged issuing easy credit consumers while the latter drove an expansion in spending.

Why does this matter for BNPL?

Credit cards were a natural, albeit more generalized, extension of the store credit system which had existed for as long as humans have been farming. BNPL is just a reskin of the store credit system, but isn’t limited to any one store. POS lending is truly a revival of the purchase plan system but with the credit risk no longer sitting with the merchant.

Interest rates are (for now) pinned to effectively 0%, the stock market is continually breaking all-time highs, and the personal savings rate is at 20-year highs. The time, then, looks right for these BNPL/POS Lending to apply the lessons learned from the previous payments innovation, credit cards, highlighted above:

Get ahead of forthcoming regulations by focusing on consumer education, support, and credit checks (otherwise defaults/missed payments will continue to rise)

Bring merchant fees in line with credit card interchange rates before merchants decline to participate and existing card networks really get up and rolling with their own installment plans

Expand network accessibility through improved POS experience (instant virtual cards)

Partner with brands & businesses to introduce reward programs to add value for consumers and increase spend

Decide whether to hold balances (see AT&T example) and offer additional financial services or develop deep partnership with established banks

My spicy take is that BNPL firms (much like Amazon and Netflix) are aiming to be the “disruptor” just long enough to drive competitors volumes/margins to unsustainable levels. This would allow the firms to set their own terms with consumers and banks all the while continuing the old way of doing things, just as a ~premium digital experience~

If you enjoyed this content please subscribe, comment, or share. If you’ve got any questions reach out to me here or on twitter!

Cheers,

Wilson