Philosophy on Payments | Part 1

Sometimes when you set out to do a simple write-up on an upcoming market event, you end up writing 25,000 words.

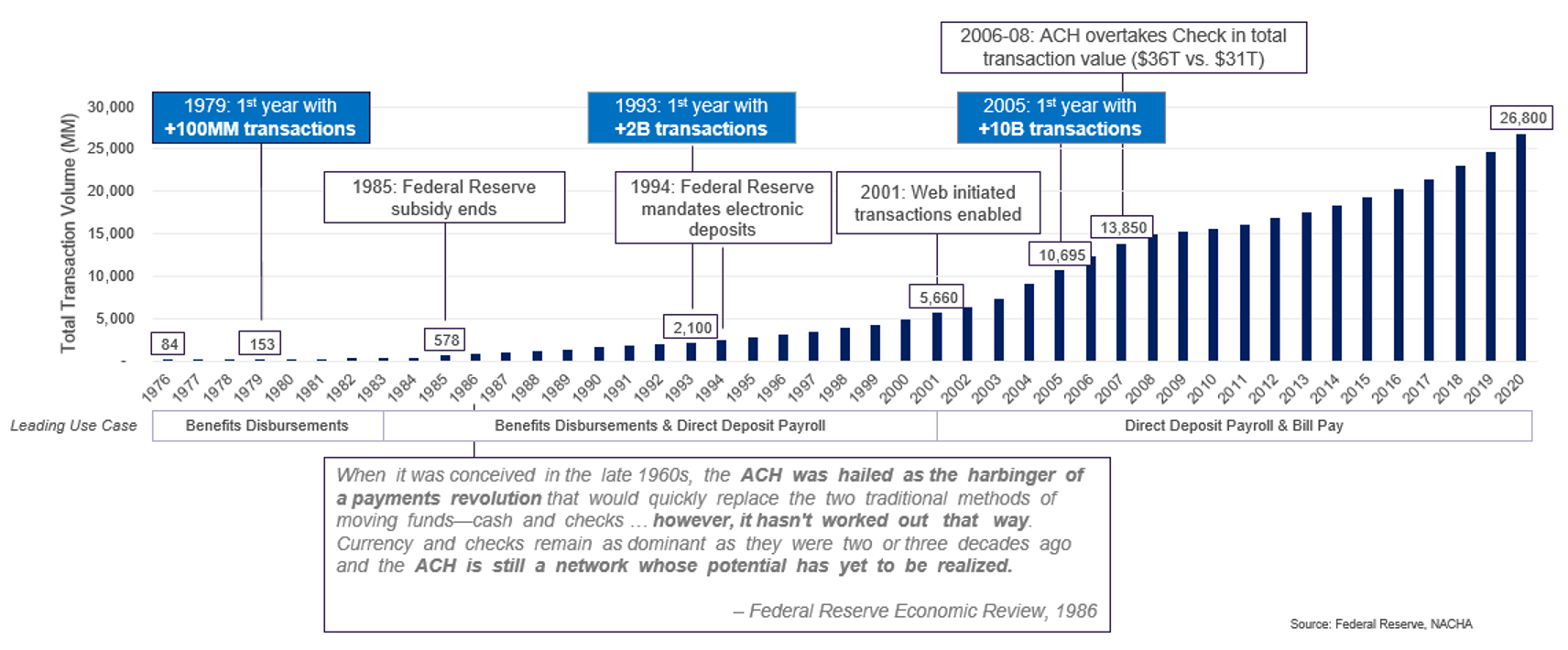

This is the most interesting and involved graph I’ve ever made:

The graph was made to show that RTP and FedNow might take many years — even decades — to gain prominence in the US. Three years later, I’m still incredibly proud of it, because it tells a story. One of growth and commitment — of people who saw things “as they were, as they are, as they might become, and as they ought to be”1 and who took the steps to influence the future.

While writing the necessary context, I identified patterns which continued to appear throughout history. The first was how trust in people and institutions compounded with each innovation in payments. This compounding increased the speed of commerce and have been engines of regional and now global economic growth.

The other patterns were less encouraging. Each innovation meant that less trust in people was required and that more trust was placed in the system facilitating the payment. The closer to the present I moved, the more abstracted transactions became, and the more people relied on trust in, what Professor Anthony Lee Zhang calls, the “Market for Promises”.

Before continuing, I want to make it clear that I am not advocating for a stateless, free-market, libertarian society. Nor am I advocating for authoritarian control and regulation. But as we’ll explore in my thoughts on how the future ought to be, these are both potential pathways.

Instead, I believe there’s a natural equilibrium of central authority involvement in payments which crops up throughout history. This essay is more akin to a historical survey with my philosophical musings sprinkled in. With that said, let’s continue.

For example, take this simplified evolution of payment methods:

Word of mouth agreements became written instructions between two parties.

Written instructions between two parties became standardized by a central authority.

The standardized payment instructions backed by an authority became transferable to people other than the transacting parties

The further away one travels from person-to-person interactions, the easier payments become, but more trust in individuals is ceded to the system. As detailed in my post on the Theory of the Firm, thinking of the system as a benevolent and homogenous thing naively assumes that the sum of human being’s actions — particularly those with authority — are going to produce the most benefit for all stakeholders.

Things today are antiquated systems and rails that move funds within our economy. The financial plumbing, which is beginning to show its age, rather than being replaced and upgraded, is having fancy modern wrappers slapped on top to manage them, in the best cases. In the worst cases, the lobbying efforts of incumbents to keep existing rails in a position of prominence actively stifle change.

From here, there naturally follows the things as they might become: slow adoption and greater intermediation driven by ever increasing complexity. The number of hands already in the payments cookie jar — acquirers, aggregators, facilitators, gateways, reconcilers, etc. — almost guarantees such that any meaningful change will take great time, cost, and effort.

But having read and written all of this, I look at things as they ought to be. I see innovations which restore some of the interpersonal trust which has been lost. Some examples that I’ll explore in greater depth:

Real-time cross border payments to help a family member.

Standardized international payments making it easy to fund a promising venture in a developing economy.

The ability to make online transactions cost less for buyers and sellers by simplifying payments

This post was originally supposed to be about things as they ought to be with FedNow, but my initial optimism and naivete quickly encountered the realities of history. Far from being discouraged, however, I have more motivation than ever to see the world move just a little closer to how it ought to be.

The spark of the post, talking about the potential lessons for FedNow, sits where things might be going. And the rest? I hope you stick around to find out.2

I’ve divided the work into four parts to be published over the coming weeks:

Things as they were — from clay tablets to RTP

Things as they are — a survey of our current ecosystem

Things as they might become — projecting current history forward

Things as they ought to be — an optimist’s view of financial innovation

I’m grateful for the brilliant scholars, practitioners, and policy makers who have lent me their writings, thoughts, and time. Any errors in logic or fact that follow are my own.

From Dee Hock’s “One from Many: Visa and the Rise of the Chaordic Organization” https://www.penguinrandomhouse.com/books/575007/one-from-many-by-dee-hock/

Maybe the real lessons are the philosophical tenets we formed along the way?