Float. Explained for Everyone.

Earlier this year, I published Payments. Explained for Everyone for my colleague Shenika. This one is for Mason and Thomas, because everyone (industry vet or curious reader) deserves to understand who profits from slow payments.

Last time, we started with a simple premise: a payment is the transfer of money. From this statement we built the three canonical payment models — the building blocks for understanding how money moves. This time, we’re going to take it a step further by following the funds around the models to define an important concept: Float.

Float is the time between the transaction starting and the final payment. It’s a feature in all payment systems. It’s used to protect buyers, sellers, and networks from fraud and reduce transaction costs. But float is also a bug in the system. It’s used to earn interest income, generate additional fees, and strategically deploy capital. Whether you think it’s a feature or a bug depends on where you sit in the system, but it’s not going anywhere — no matter how fast payments get.

Float explains the reason businesses still mail checks or the reason Warren Buffett and Mohnish Pabrai got so rich. By the end of this, you’ll at least understand why.

Follow the Message and Money

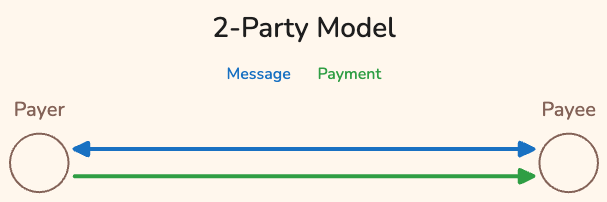

There are two parts of every transaction: the message (“I want to buy this”) and the final movement of money. What’s important to understand is that these two are separate events. When these events happen at different times, then float is introduced. Where float exists, value will accrue.

Note: The rest of this will cover the payment, but you should know that messages are subject to the similar flows and constraints. But the difference between Authorization, Clearing, and Settlement messages is best saved for another time.

We’re going to straighten out the canonical payment models to follow the money and the message then see where it slows down. When we do this the models look like a supply chain1 that moves money and messages between the payer and the payee.

In a 2-party system, the value of float benefits only the payer. The money is still in the payer’s pocket as inventory, and the payee must wait or borrow funds to spend the money from the transaction. Think of it like eating out with your friend and putting the meal on one ticket. When you pay, you are “floating” the cost of their meal until your friend pays you back.2

This is a central tension in payments: no one wants to pay out faster, but everyone wants to be paid right away.

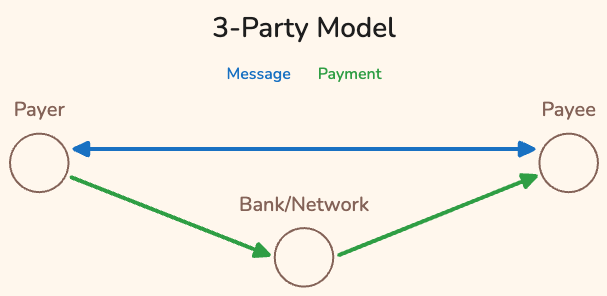

3-party systems follow the same idea, but now float could benefit the payer or the bank. The biggest change is in the 3-party model the bank/network could choose to introduce float, hold the funds, and generate additional value.3 This change compounds the tension of paying slow vs. being paid fast.

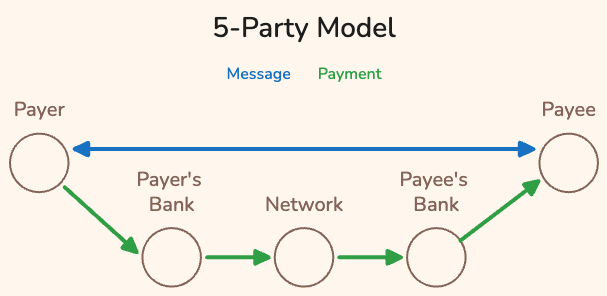

The 5-party model is subject to the same challenges as the 3-party system, except now there are two additional parties who have an incentive to move slow.4 As a general rule, the further up you are in the transaction supply chain, the more you stand to benefit from float.5

So we should abolish float?

At this point, you might be asking: why doesn’t everyone just maximize float? Why do we settle transactions? The short answer is the economy would collapse. If no one ever settles a transaction, no one would ever have money to spend → a bunch of boxes sitting idle in a warehouse is no use for anyone.

The longer answer is that there are controls to prevent intentional delays and limit how much float inventory a party can generate. These controls are generally set by network operators, legislators and judges who set/enforce regulations, and competitive market forces.6

But float isn’t all about greed and accumulating inventory. It keeps payments safe and low-cost. Moving slower lets us ask “is this a valid transaction?” and take action before the money moves. Slowing down also allows allows for netting (offsetting inflows and outflows) and batching (grouping like payments) to reduce the cost of transactions.7

To understand how companies actually use float, let’s return to our opening examples:

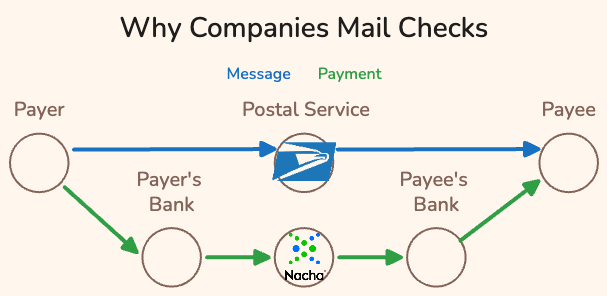

Why do companies still mail checks?

Companies still send paper checks because they want to keep money in their accounts for as long as possible. Mailing a check stretches the float by adding the time it takes to get the letter from the payer to the payee. This works in the U.S. and UK because of the “mailbox rule.”

This rule deems a payment made on the date the postmark is stamped on the envelope — even if the payment is physically received days later. In practice, this means that if your bill is due on the 15th and your envelope is postmarked by the 15th, you’re on time — even if it lands on the 20th. The payor gets five days of free float on top of the time it takes to process the check.

Multiply that across thousands of monthly payments and it becomes a deliberate cash management strategy, rather than a quirk of the postal system. Payees know this, which is why they’ll stipulate payment terms in contracts that require the check to have arrived by the payment date or specify a less float-friendly payment method like ACH or wire transfer.

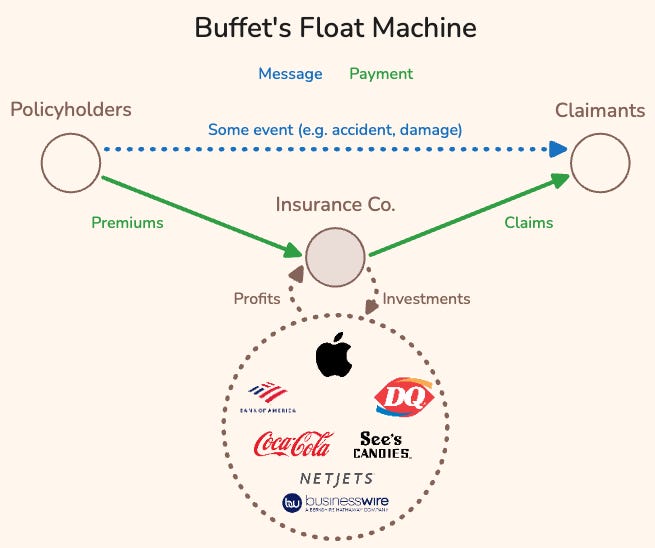

How did investors like Buffett & Pobrai build empires on float?

And why don’t all insurers do this?

Insurance companies are natural float factories: they collect premiums upfront and pay claims later, sometimes years later if at all. These companies succeed in making sure that premium inflows are greater than claim outflows through underwriting the risk of events (accidents, damages, etc.). Insurers can also generate profits by investing the float they naturally generate.

Traditional insurers invested the float in safe, low-return assets: government bonds, treasuries, and corporate debt. Buffett (and later Pobrai) saw opportunity by taking a different approach. Berkshire Hathaway bought insurance companies like GEICO & National Indemnity in the 1960s and 70s. Rather than bonds, he invested it in companies like Coca-Cola, Apple, and all the other companies in Berkshire’s portfolio.

By 2025, Berkshire’s float had grown from $16 million in 1967 to $176 billion. This capital base functionally pays for itself through “underwriting profits.” Most insurance companies are not generating underwriting profits, so they don’t have the luxury of investing in risky assets. This strategy only works because Berkshire’s insurance arm is great at pricing risk. So while most of their competitors are borrowing capital at market rates, Buffett is getting paid to use his. All thanks to float.8

This post added to the 2-, 3-, and 5-party models by splitting the payment into two parts: a message and a transfer. We saw how float, the delay between message and transfer, can impact different parties. You now have the language to describe float, and there’s so much more to get into — things like bridge financing, EFTA Reg E, and message authorization. These are all stories for another time.

If you want to dive deeper, check out Who Profits from Slow Payments. If you have any questions or think I left anything out, let me know in the comments or by replying to me!

The visualization of this was originally going to be a river, and I may return to it at some point. However, just before publishing, I read Mason Reeve’s excellent post on “cloud clearing” and the future of transaction clearing/processing.

In it, He briefly calls float the “processor’s inventory,” and I realized that metaphor fit better here — it also ties nicely into my previous work on logistics metaphors in payments:

You may not be this way, but we all know people who do this.

Some examples include:

Extending float as a service to the payer in the form of credit → 30 day repayment term

Protect the payer and bank from fraud losses → inspection & quality control

Holding the funds to generate interest income → inventory holding fees

Charge the payee a fee for faster access to their money → rush delivery

All of these are examples of the “Principal-Agent Problem”: Any time a principal (payer or payee) delegates decision making (how quickly to move money) to an agent (bank, network, processor), there is a risk that the agent doesn’t act in the best interest of the principal. More on that here.

This is a gross oversimplification. There are many situations where a slow payment can harm a payer like pay-on-delivery, penalty deadlines, etc. This is why things like 30-day payment terms and working capital financing exist. It’s also why so many fintechs and lenders exist to help shrink or “bridge” the float gap.

Rules: Networks (NACHA, SWIFT, cryptocurrencies) will set minimum processing or availability requirements for participants. If you don’t comply, you might get fined or kicked out of the network altogether

Regulations: Laws may be put in place to force early payroll if payday falls on a weekend, Monday, or holiday. Other laws allow payers/payees to take banks to court. If a payer refuses to pay, they may be sent to collections

The Electronic Funds Transfer Act deserves its own post and deep dive on how and why it was developed. It’s one of the most foundationally pieces of legislation in the US payments industry. Yet, most of us know very little about it aside from seeing “Regulation E” on some of our statements (if we read them at all).

Competitors: Any of the parties involved might switch to a new bank or network if delays or terms are seen as excessive. Stripe lost some merchants to firms like Adyen and Checkout.com when it changed holding period requirements in 2020.

Of course, almost every merchant acquirer raised reserve requirements in 2020. Reserves are used to cover things like returns, exchanges, and chargebacks. This is particularly important in online shopping where shoppers are 2-3x more likely to return or exchange an item and experience ~5% more fraud than in-store. With everyone stuck at home and shopping online, processors were on the reverse end of the float challenge — they had to pay back the payer while trying to recover funds from the merchant.

There’s debate on weather investing float in speculative assets violates the principles of asset-liability matching (ALM). If you have a low-probability liability (damage, injury) that could be called on at any time, then you want to pair it with an investment that holds similar value and is sufficiently liquid (bonds). Equity investments — particularly private equity — have higher risk/volatility than bonds. When managed well (as with Buffett), things go great. However, if mismanaged, it can sink the entire company.